Your mortgage could be doing more than just getting smaller. Here’s how smart loan structuring can accelerate your path to financial freedom — explained by your local mortgage broker.

If you own a home in the Hills District — whether it’s a family house in Castle Hill, a townhouse in Bella Vista, or a newer build in Box Hill — chances are your biggest financial asset is sitting right beneath your feet. And if you have a mortgage, you’re already on the right track. But what if that same loan could be structured in a way that helps you pay it off faster and build long-term wealth at the same time?

That’s the idea behind debt recycling — one of the most talked-about strategies among Australian homeowners right now, and one we’re increasingly helping Hills clients explore at Gain Home Loans.

Let me be clear from the outset: debt recycling sits at the intersection of mortgage structuring and investment strategy, so it requires input from both your mortgage broker and your accountant. My role — and what I’ll focus on here — is the loan structuring side: how your home loan can be set up to make this strategy possible.

So, What Exactly Is Debt Recycling?

At its core, debt recycling is a strategy where you systematically convert non-deductible debt (your home loan) into deductible debt (money borrowed to invest). The end goal is to reduce the total interest you’re paying on your home over time while building an investment portfolio alongside it.

Here’s a simplified version of how it works: as you make extra repayments on your home loan and build equity, that equity is accessed and redirected into income-producing investments — typically shares or managed funds. The interest on money borrowed to invest can potentially be tax-deductible (your accountant will confirm this for your situation), which makes the debt “good debt” in the eyes of the tax system. Over time, the non-deductible home loan shrinks, the investment portfolio grows, and your financial position improves on both fronts.

“The goal isn’t to take on more risk — it’s to make your existing equity work smarter, while keeping you on track to pay off your home faster.”

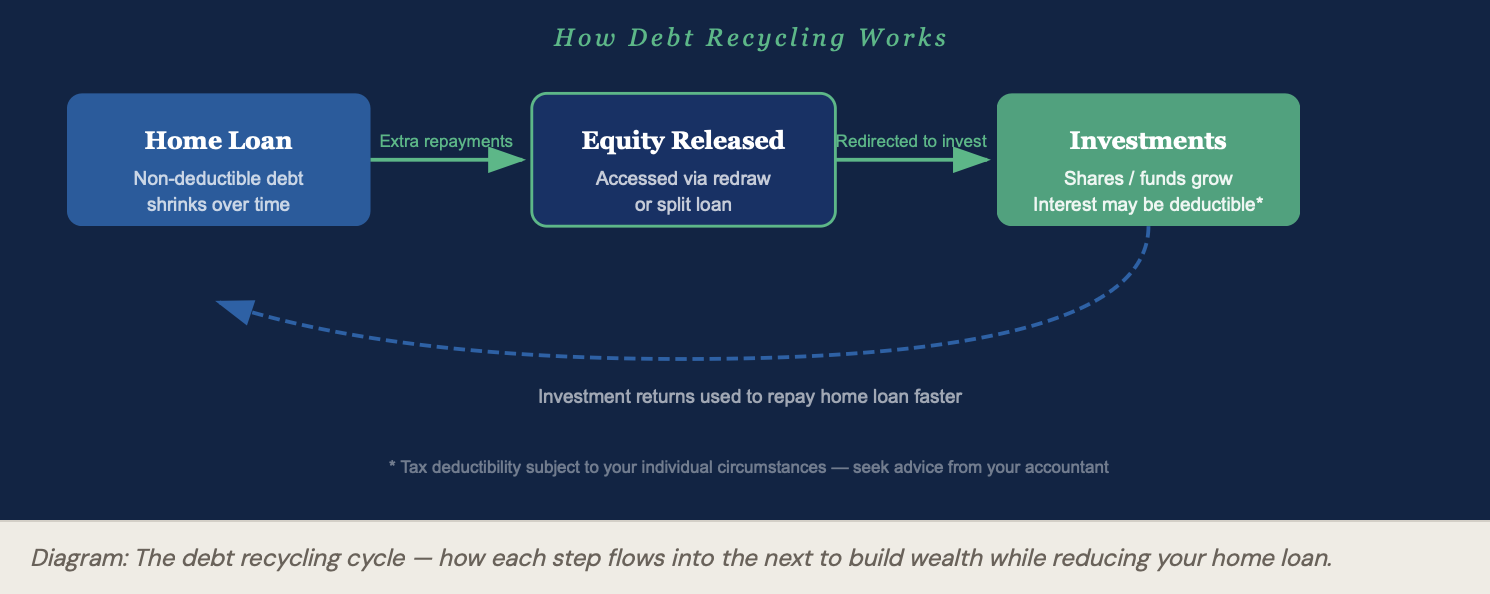

How Debt Recycling WorksHome LoanNon-deductible debtshrinks over timeExtra repaymentsEquity ReleasedAccessed via redrawor split loanRedirected to investInvestmentsShares / funds growInterest may be deductible*Investment returns used to repay home loan faster* Tax deductibility subject to your individual circumstances — seek advice from your accountant

Diagram: The debt recycling cycle — how each step flows into the next to build wealth while reducing your home loan.

The Loan Structure That Makes It Work

This is where a good mortgage broker earns their keep. Debt recycling doesn’t work with just any loan — the structure needs to be right from day one. Here’s how we typically set it up:

- An offset account or redraw facility on your home loan. Every extra dollar you put into your offset reduces the interest you pay — immediately. Over the life of a Hills mortgage (which can easily be $800K–$1.2M+), even modest extra repayments make a significant difference.

- A split loan structure. We separate your home loan into two portions: the original home loan (which you continue to pay down), and a new investment loan drawn against your equity. Keeping these completely separate is critical for record-keeping and tax purposes — your accountant will thank you.

- An investment loan (interest only, typically). The new portion of debt is drawn down progressively as you build equity, and used specifically for income-producing investments. Because the purpose of this loan is investment, the interest on it may be tax-deductible — again, seek your accountant’s advice here.

- Regular review points. As your property value changes and your loan balance reduces, the strategy needs to be revisited. We build this into the process with regular loan reviews — something we do as standard for all Gain clients.

The beauty of this structure from a lending perspective is that it accelerates your home loan repayment. The returns from your investment portfolio — dividends, distributions — can be used to pay down your home loan even faster, creating a compounding effect over time.

Is Your Home Already Primed for This Strategy?

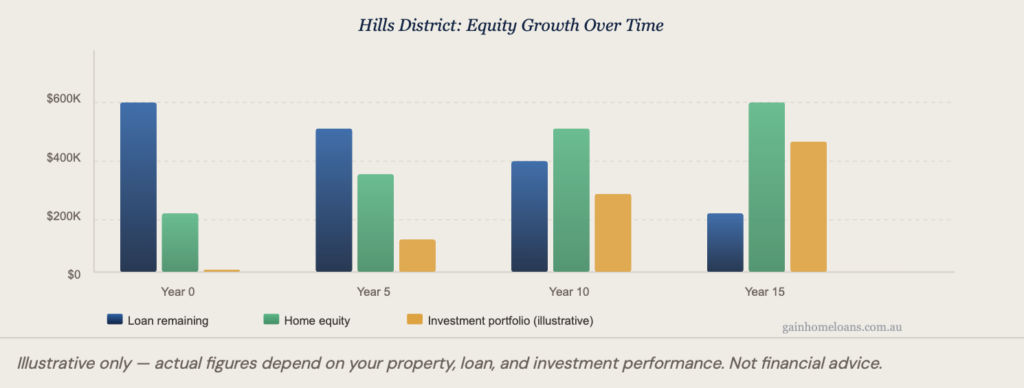

Given the strong property growth the Hills District has seen over the past several years, many homeowners in suburbs like Kellyville, Rouse Hill, Baulkham Hills, and Norwest are sitting on considerable equity — often without realising just how much. The question isn’t whether you have the equity; for many Hills families, you do. The question is whether that equity is being put to work.

Generally speaking, debt recycling tends to suit homeowners who:

- Have a stable income and can make consistent extra home loan repayments

- Have built meaningful equity in their home (typically 20% or more)

- Have a long-term investment time horizon (10+ years)

- Are comfortable taking on some investment risk in exchange for potential long-term gain

- Have — or are willing to engage — a good accountant and financial adviser alongside their broker

It’s not right for everyone, and that’s an honest answer. Your personal circumstances, tax position, risk tolerance, and financial goals all play a role. But for the right Hills homeowner, it can be genuinely transformative.

The Role of Your Accountant — And How We Can Help Connect You

One of the most common barriers we see is that people have a broker, and they have an accountant, but the two are never in the same room together. Debt recycling really does require those two conversations to happen in sync.

At Gain Home Loans, we work with a network of trusted, Hills-based accountants who understand property and investment lending strategies. If you don’t currently have an accountant — or if yours isn’t across this area — we can facilitate a one-to-one meeting with our in-house accounting contact. You sit down together, we walk through the loan structuring options, and they advise on the tax implications. It’s a joined-up conversation that, frankly, most people never get to have.

All you need to do is give us a call, and we’ll arrange it from there.

BROKERACCTLoan structureSplit loan + offsetTax strategyDeductibility adviceYOU”A joined-up conversation that most people never get to have.”Call Gain Home Loans to arrange your complimentary broker + accountant consultation

The Gain Home Loans approach: we bring your broker conversation and your accounting conversation into the same room.

A Quick Word on Paying Off Your Loan Faster

Even if debt recycling isn’t the right strategy for you right now, the loan structuring principles behind it are worth knowing — because they apply to anyone who wants to pay off their mortgage faster.

Paying fortnightly instead of monthly. Using an offset account properly (and not treating it like a spending account). Structuring a split loan so part of it is variable and responsive to extra repayments. Making sure your rate is competitive — because paying an extra 0.5% on a $900K loan is over $4,500 a year in unnecessary interest.

These aren’t complicated strategies. But in our experience, most Hills homeowners are not using all of them — often simply because no one has sat down and reviewed their loan with this lens. A loan structure that made sense in 2019 may not be the most efficient structure in 2026’s rate environment. We do free loan reviews, and more often than not, there’s something worth improving.

Ready to Find Out If Debt Recycling Could Work For You?

Give us a call or send us a message. We’ll review your current loan structure, discuss your goals, and — if you’re interested in exploring debt recycling — connect you with our in-house accounting contact for a one-to-one strategy session. No obligation, just a straight conversation.